Growing old, becoming disabled, or suffering from a serious medical condition can upset your financial security, potentially leaving you in thousands of dollars of debt. While you were at one time able to pay your credit card bills in full, you may find yourself unable to keep up with future repayments, your debts spiraling due to medical bills combined with the loss of income. All the while, unofficial inflation raises the cost of food, utilities, and other essentials. Even for those lucky enough to stay healthy, the cost of living rises as the years go by. And then the debt collector calls begin…

Here’s the Good News – You Need Not Tolerate Senior Citizen Debt Collector Harassment

Forty years ago, Congress passed the Federal Debt Collection Practices Act (FDCPA) to protect you from the “use of abusive, deceptive, and unfair debt collection practices by many debt collectors.” This law makes it illegal for a debt collector to harass you. It also gives you certain rights, including the right to sue the debt collector for damages. Many states now have similar laws.

How do Debt Collectors Use Harassment Against Elderly and Disabled People?

According to a 2020 FBI report, “approximately 28% of the total fraud losses were sustained by victims over the age of 60, resulting in approximately $1 billion in losses to seniors.”

The list of sneaky debt collector tactics exceeds the number of items on most hospital bills. AARP recently identified four new illegal schemes:

The Hospital Hustle: Shortly after your emergency admission a debt collector, who wants you to believe they work for the hospital, tells you to either pay prior hospital bills or go elsewhere for care. Don’t pay. Tell them that federal law requires hospitals to provide emergency care regardless of unpaid bills.

The Credit Card Capture: You have a credit card debt now noncollectable due to the statute of limitations (Note: the statute of limitations varies by state). Here’s how the trick works: A debt collector who’s after that expired debt forms a partnership with a bank, which then offers you a credit card. You take the offer not knowing that the fine print in the new card agreement provides that part of your first payment will apply to the old debt. This small payment will bring the old debt, with all accrued interest, back to life.

If you have past debts, think carefully about accepting new credit cards.

False Facebook Friends: Debt collectors use fake profiles to befriend their targets, impersonate real “friends”, or engage in harassment, such as posting messages advertising that the person owes a debt.

Keep your private information off social media.

High-mileage hoaxes: Posing as law enforcement, the crooks phone their targets (regardless of whether debts are owed) and threaten arrest unless debts are paid. This scheme gets its name from the location of the debt collectors – they claim to be monitoring their targets from just blocks away, ready to pounce, but are in fact located in call centers across the globe.

The AARP also warns against these frequent abuses:

Threatening to take Social Security or Veteran’s Benefits. These can only be taken for a state or federal debt.

Demanding debts of a deceased spouse. These debts belong to the deceased’s estate, not to you.

Using repeated calls, offensive language, and other forms of harassment to force you to pay a debt whether you owe it or not.

Threatening to immediately take your possessions and send you to jail.

In addition, an Elderly or Disabled Person Can Protect Themselves with These Actions:

There are templates for appropriate letters created by the federal Consumer Financial Protection Bureau (CFPB). These are provided here along with further assistance. One of these letters requests that the debt collector not contact you again. They must honor your request, with two non-threatening exceptions.

Buy a notebook and keep it near your phone. Document every call. Keep copies of every letter and all correspondence.

Do not pay anything on old debts, debts that are not yours, or debts you cannot confirm.

Stay connected with tech-savvy family members who can help you avoid elderly scams by filtering out typical scam calls.

If you are harassed, do not endure it. Contact an experienced consumer protection lawyer to help you.

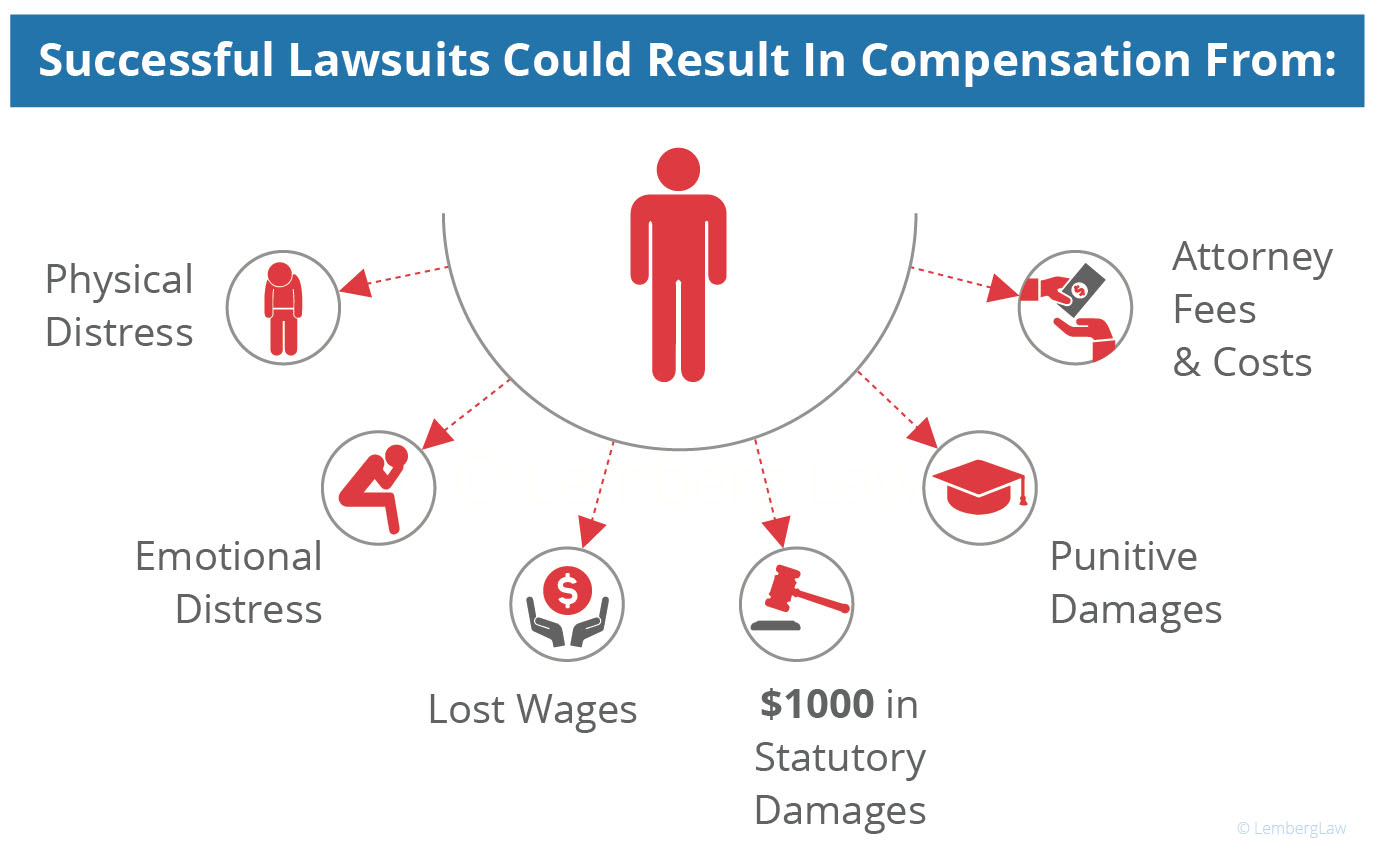

If you want to sue the debt collector for your injuries, you should have a consumer protection attorney represent you. You may be entitled to the following monetary remedies:

Physical distress caused by the debt collector’s illegal action.

Emotional distress caused by the debt collector’s illegal action.

Lost Wages.

Wage garnishment recovery.

$1,000 in statutory damages.

Punitive damages.

Payment of your attorney fees and costs.

If a debt collector has been hounding you, call 844-685-9200 now for a free, no-obligation case evaluation with one of our representatives. Our attorneys have experience fighting debt collectors and standing up for consumers. If a debt buyer has violated the Fair Debt Collection Practices Act, you’re entitled to file suit in federal court and could be awarded up to $1,000 and other damages.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."

Phone call unwanted and credit calling.