Does Unpayable Medical Debt Threaten the Average American Family’s Future?

Say you’re part of an average American family of four with zero medical debt. Between combined spouses’ earnings, you pay your bills regularly and save a little each month towards a house or some other family dream. But unexpectedly, Carlos breaks his leg, or Anna needs braces. Dad comes down with appendicitis or Mom falls pregnant. All of a sudden, medical bills appear on the horizon. Your employer’s insurance company pays part of them, but surprisingly high deductibles quickly deplete your savings and eat into your monthly income, leaving you with difficult choices as to who gets paid.

Why is this happening? No, it’s not your fault. Healthcare costs and deductibles have rocketed in recent times, and around one-third of American families share your medical-debt pain.

World’s Highest Health Costs Propel Medical Debt Ever Upward

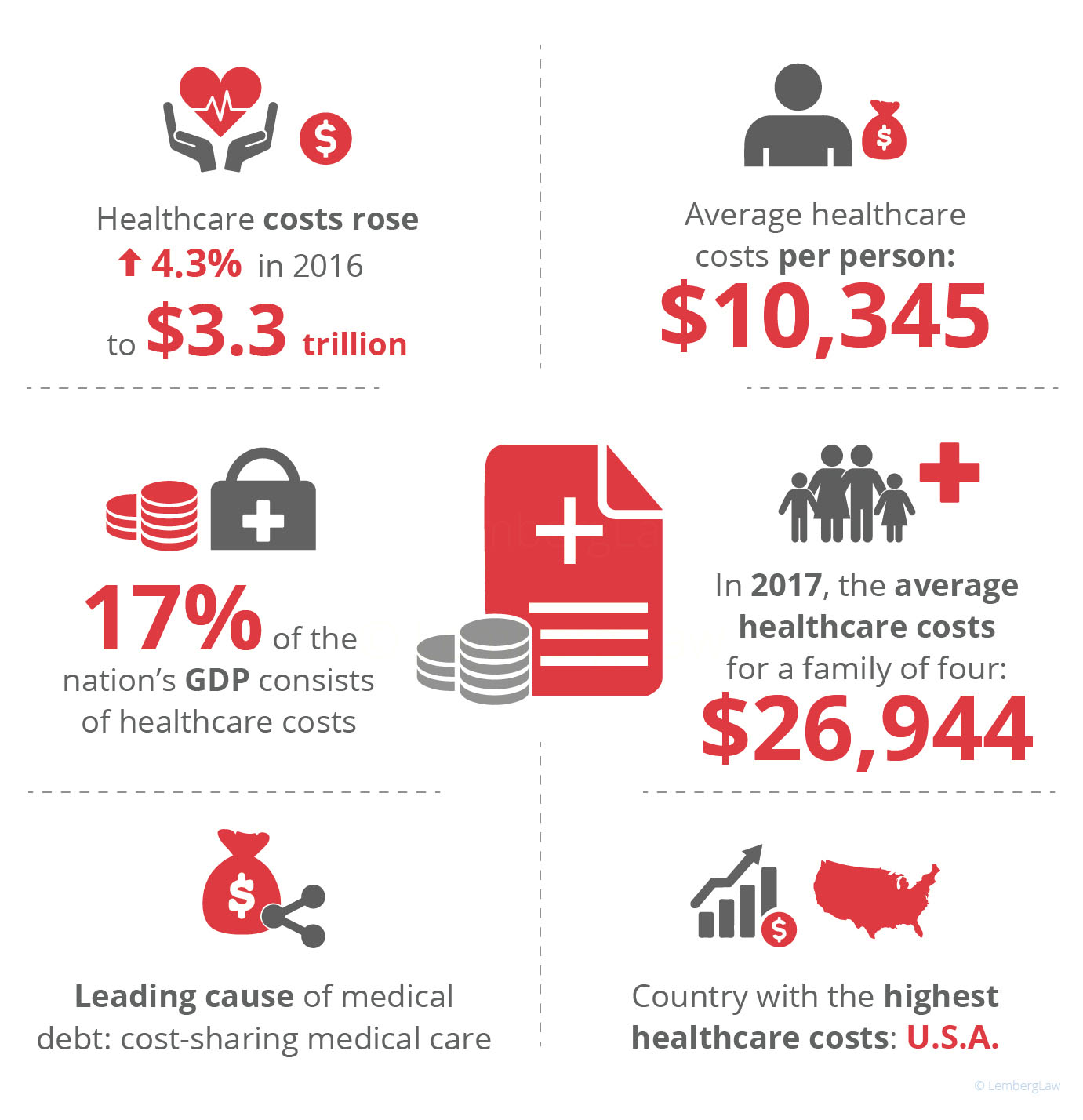

In 2016, U.S. healthcare spending increased 4.3 percent to $3.3 trillion, or $10,348 per person. Healthcare spending represents 17.1 percent of our GNP, almost twice the average of all other countries. Higher charges for care, patients getting more intense and expensive care, and a population that is both growing and aging have all contributed to the spending increase, according to a recent study by the Journal of the American Medical Association (JAMA).

According to a position paper from GenFKG, a financial training organization for millennials, healthcare cost increases are unsustainable and will continue to rise without significant public-policy changes. This demands exceptionally courageous action by our politicians.

For the Average American Family, Decreasing Insurance Benefits Mean Increasing Medical Debt

A recent study, “Medical Debt Among People With Health Insurance” by the Henry Kaiser Family Fund, found that medical debt occurred in families of all ages with incomes ranging from $10,000 to more than $100,000. Other key findings include:

Among insured individuals, unaffordable medical debts resulted primarily from cost-sharing of care covered by their insurance.

Out-of-network charges also proved burdensome.

Coverage limits and exclusions along with unaffordable premiums also caused problems.

Related problems can often exacerbate medical debt.

Once it starts, medical debt can be hard to stop.

Medical debt can trigger other severe consequences.

Tips for Managing Medical Debt

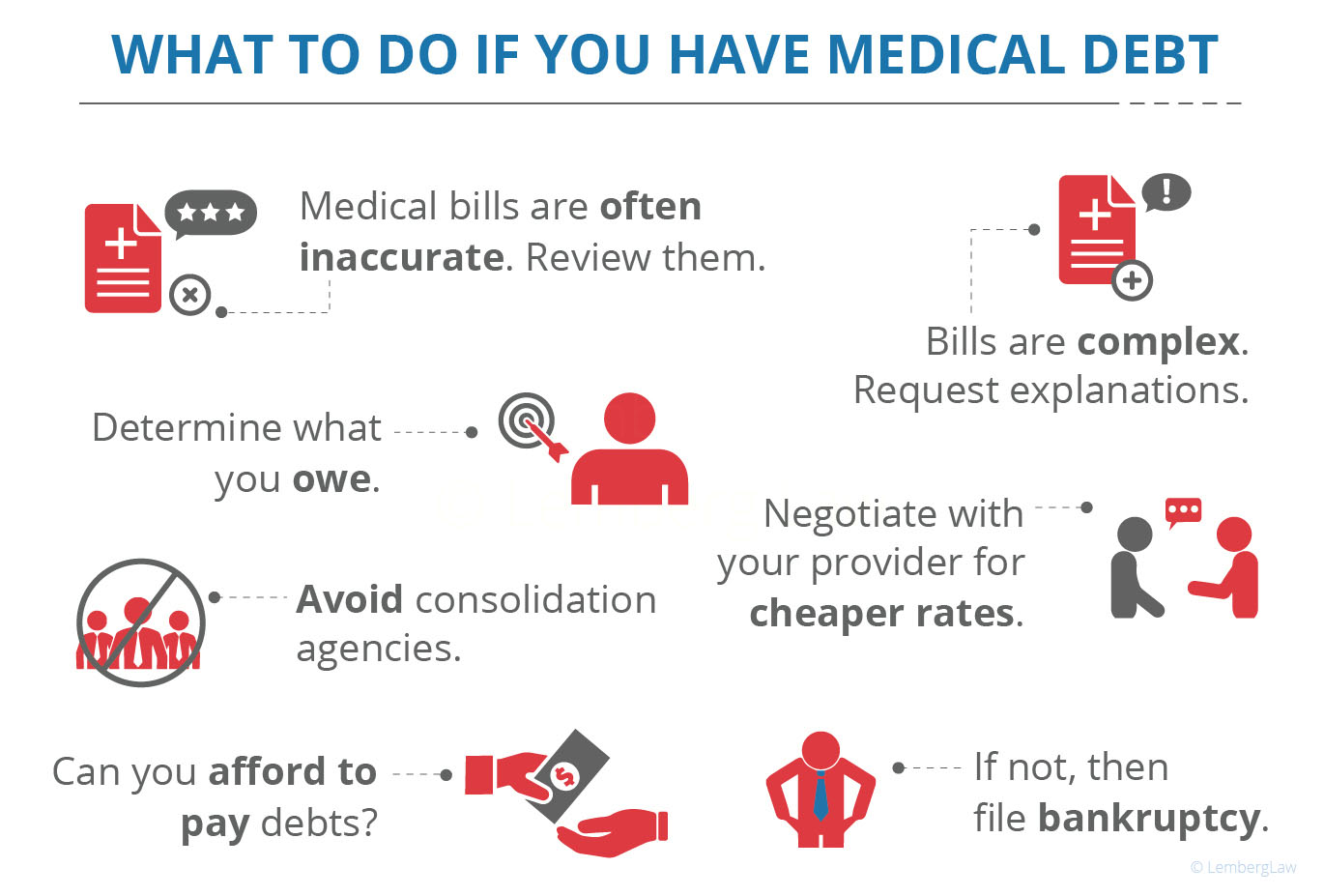

There is no easy path or single way to manage the bills that follow your medical event, but a financial crisis will strike if you do not manage the payment in a manner that fits you and your family. Determine What You Owe

It will be easier to keep up than to catch up. Begin managing the bills as soon as you are able.

Do not assume all the bills are accurate since medical bills are notoriously inaccurate. You will receive multiple bills and statements from your insurance company, and it may be very difficult to reconcile them.

Make sure you understand the charges. Many providers use a code which is hard to decipher.

If you do not understand the charges, demand an explanation from the provider and a corrected bill if appropriate. If the bill has many charges, you may want to review it with a billing specialist at the hospital.

Create a detailed paper trail of what you do and what you are told.

Determine If You Can Pay

Negotiate with the provider. Ask the provider to charge you the amount that it would charge an insurance company, which is generally much lower.

Negotiate a written payment plan that works for you. Providers often accept low monthly payments.

Learn if you qualify for assistance from a federal program (click here for more info), or by contacting your state’s social services department.

Can you afford to pay the bills? Examine your financial circumstances to determine if you can pay, for example, from savings or by temporarily eliminating non-essential expenses, applying for a bank loan, paying off your medical debt with a credit card, securing a home equity loan or line of credit, or by seeking out a medical debt consolidation loan.

Beware of debt consolidation agencies. They often charge high upfront fees for promised services they cannot deliver.

File bankruptcy.

Watch Out for Medical Debt Collectors

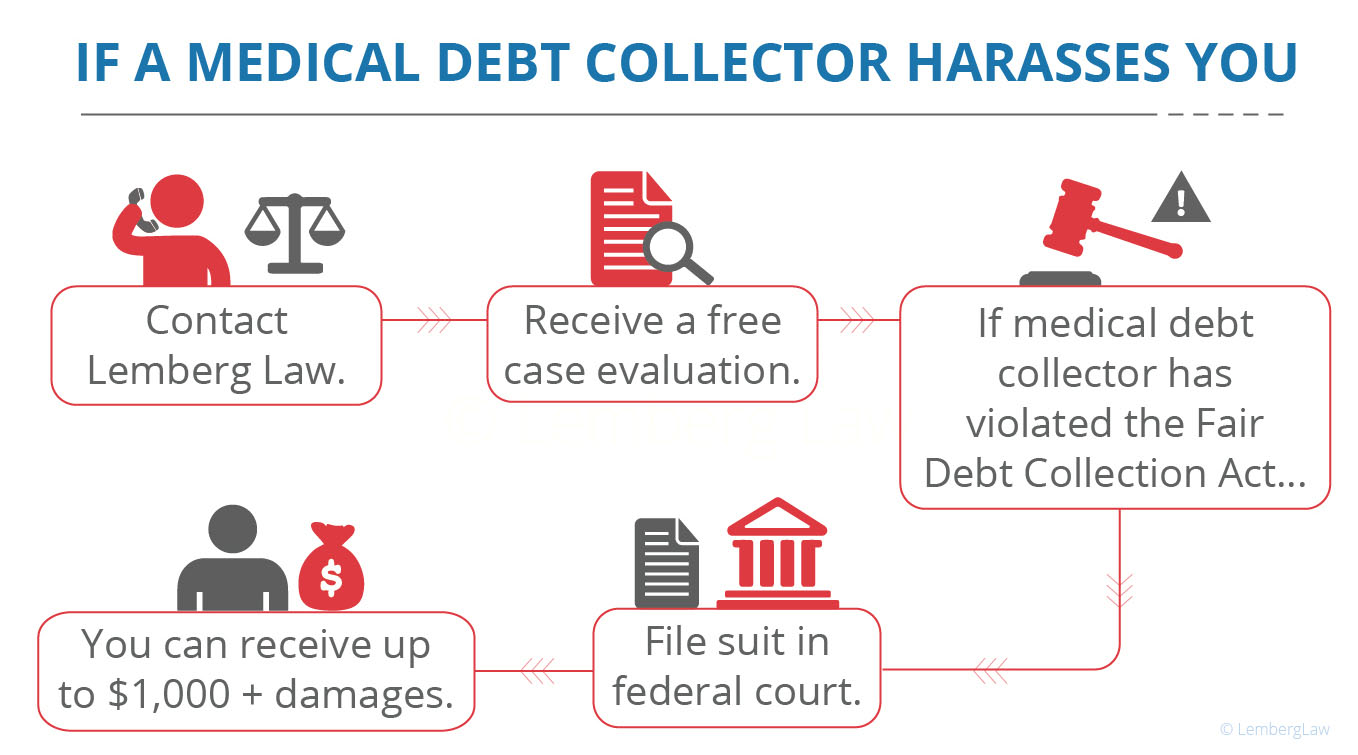

Hospitals and doctors often give unpaid debts to debt collectors after 60 to 90 days. The Federal Debt Collection Protection Act protects you from medical debt collector harassment such as repetitious phone calls (including robocalls) that are intended to annoy, abuse, or harass you or any person answering the phone, as well as obscene or profane language, and threats of violence or harm.

If a medical debt collector has been hounding you, call 844-685-9200 now for a free, no-obligation case evaluation with one of our expert representatives. Our attorneys have experience fighting medical debt collectors and standing up for consumers. If a medical debt collector has violated the Fair Debt Collection Practices Act, you’re entitled to file suit in federal court and could be awarded up to $1.000 and other damages.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."