Did you know that if there’s an error on your credit report, you’re the one that’s responsible? This can be problematic considering that many businesses buy credit reports to help them make important decisions about them.

What Is a Credit Report?

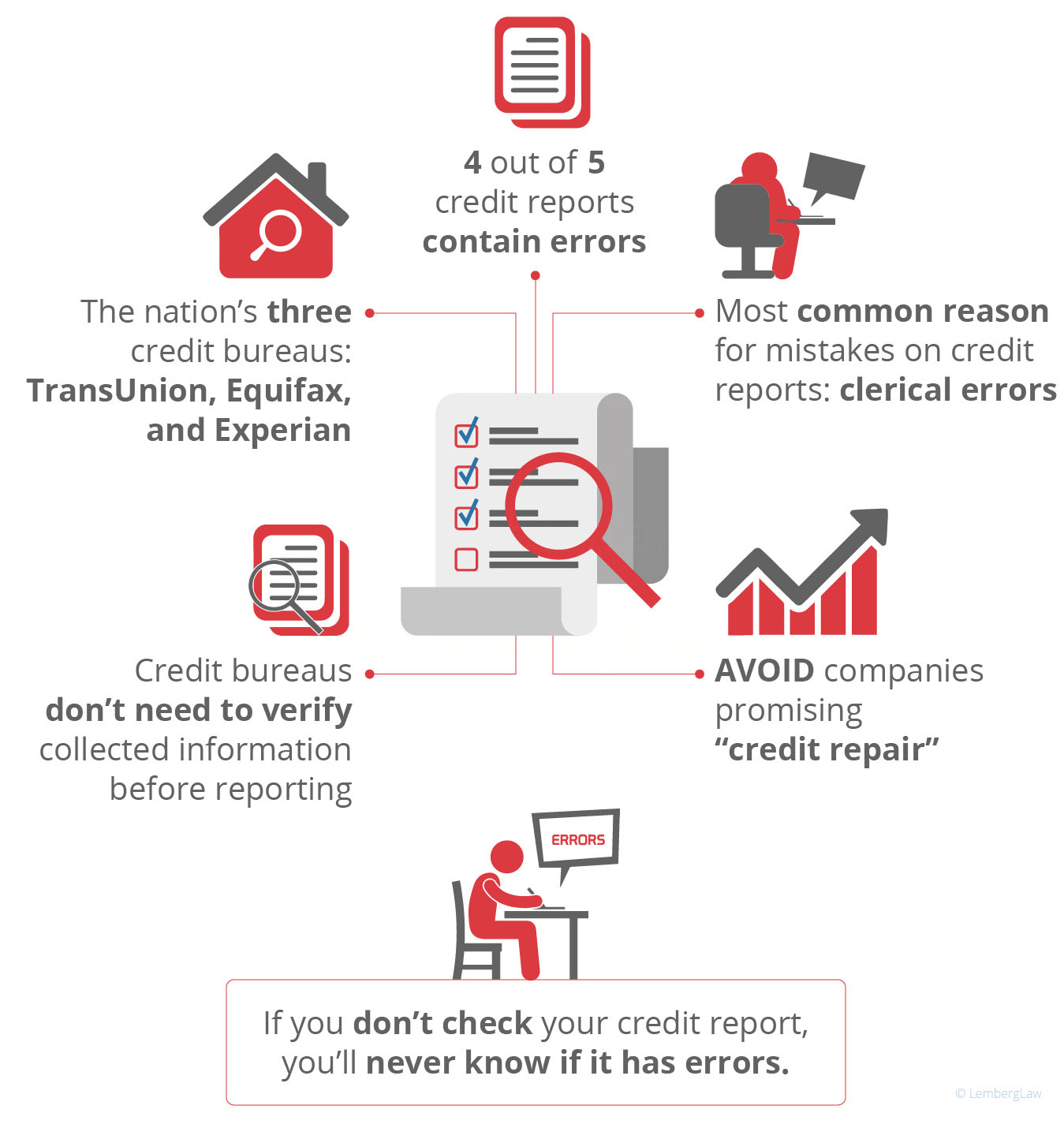

Credit reports are nationwide statements of your credit history created by a credit bureau. TransUnion, Equifax, and Experian are the three credit bureaus in the nation. They produce these reports by collecting information from public records and creditors. Then they profit from selling this information to businesses.

What Are Credit Report Errors?

The most common errors on credit reports are typically inaccurate, incomplete, or duplicated information. This is not due to malicious intent, but often because of a clerical error. Every bureau contains an individual report that they collect from you independently.

Be aware that there exist no laws requiring credit bureaus to confirm information they have collected on you before they report it. As a result, there are often conflicting credit reports that contain errors. It is concerning, and you should be cautious because mistakes like this commonly occur.

How Can You Find Out If Your Credit Reports Has Errors?

You have to check your credit report. Otherwise, you may never know if it has errors. It is now easier to do this because of recent legislation.

Every person is entitled to a Free Annual Credit Report. You may receive one copy of your credit report, once every 12 months, from the credit bureaus as a result of an amendment to the Federal Fair Credit Reporting Act. It’s easy to receive your free credit report from one or all of the credit agencies within 15 days. You can also call them at 877-322-8228.

Why You Should Dispute Credit Report Errors

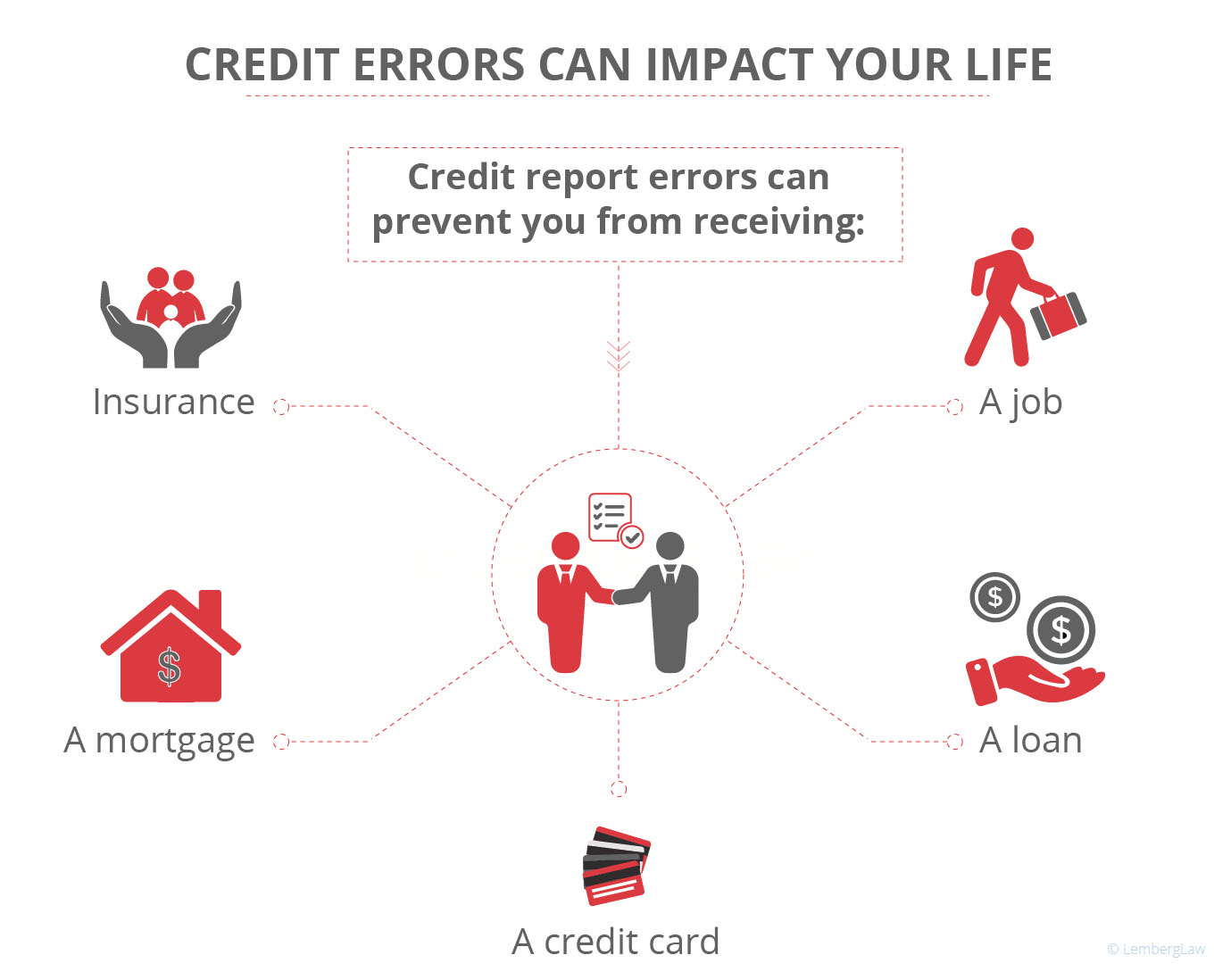

Be aware and make sure your credit reports are accurate. If you find an error, you need to report it. Credit report errors aren’t something to take lightly. An error on your report can prevent you from receiving insurance, a mortgage, a credit card, or a loan. Some mistakes can even keep you from getting a job. Be aware and make sure your credit reports are accurate. If you find an error, you need to report it.

Consumers need to be aware of any “credit repair” promises. The FTC notes that these programs offer false promises. They add that consumers are entirely able to do these tasks for little to no money.

How to Correct Credit Errors

The Fair Credit Reporting Act is a federal law that holds the organization that provided information about your credit history and the credit bureau accountable for incomplete or incorrect information on your report. If you need to have errors fixed, follow the Federal Trade Commission’s advice:

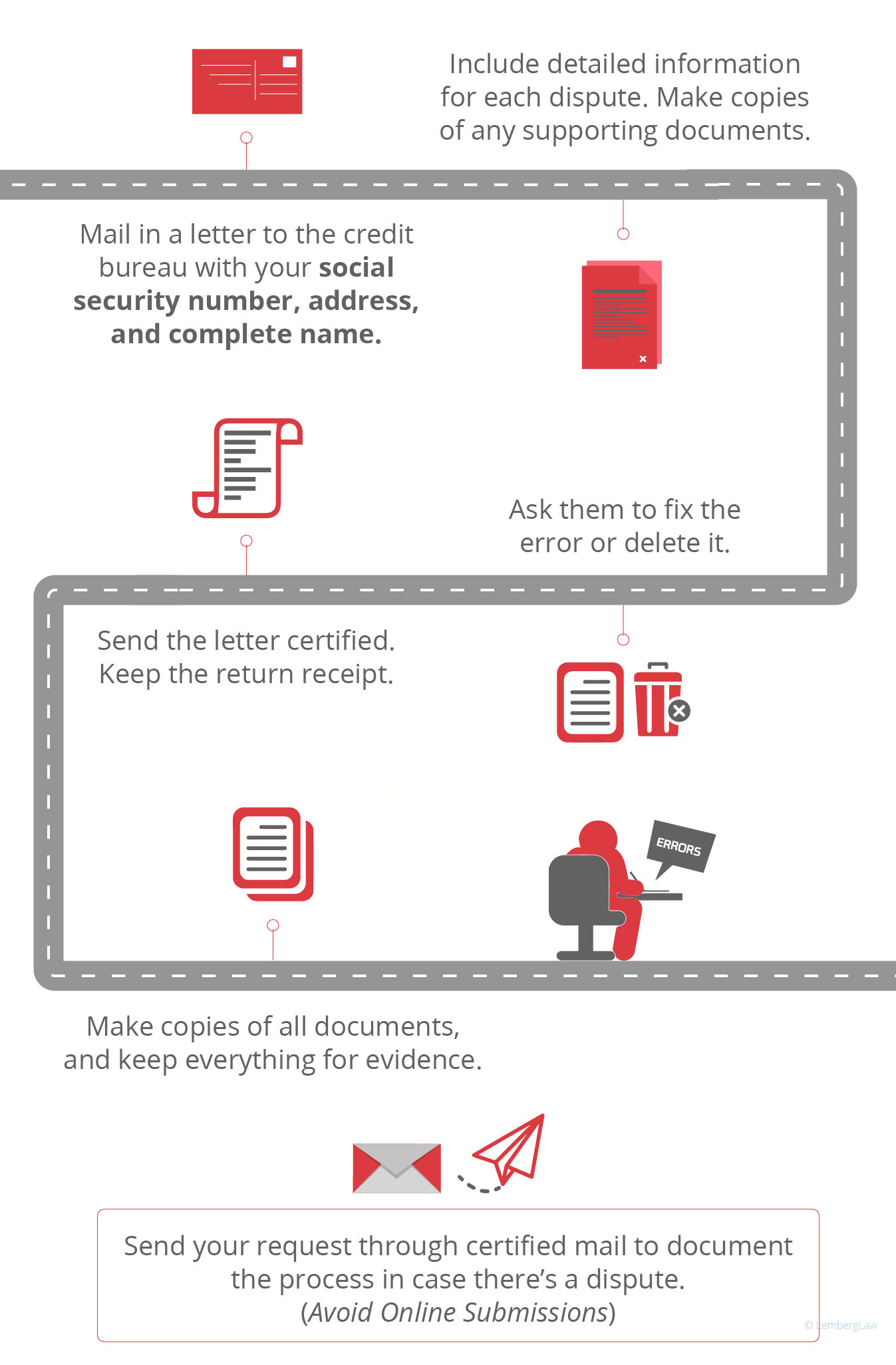

Mail in a letter to the credit bureau with your social security number, address, and complete name.

Include detailed information for each item you’re disputing. You will also need copies of any supporting documents.

Ask them to fix the error or delete it.

When you mail the letter, send it certified, and hold onto the return receipt.

Make copies of the letter and hold onto everything for evidence.

While you can fill out an online form on the credit bureau’s website, you want to send your request through certified mail to document the process in case there’s a dispute.

Credit bureaus must follow a specific process when you make a dispute. They must investigate all disputes, unless they are considered frivolous, typically within 30 days. All of the data you sent them must be forwarded to the information provided by the bureau.

The creditor or other organization must investigate the claim, review all information they have received, and report their findings to the bureau. They must either correct your file or notify the bureau that the disputed information is inaccurate.

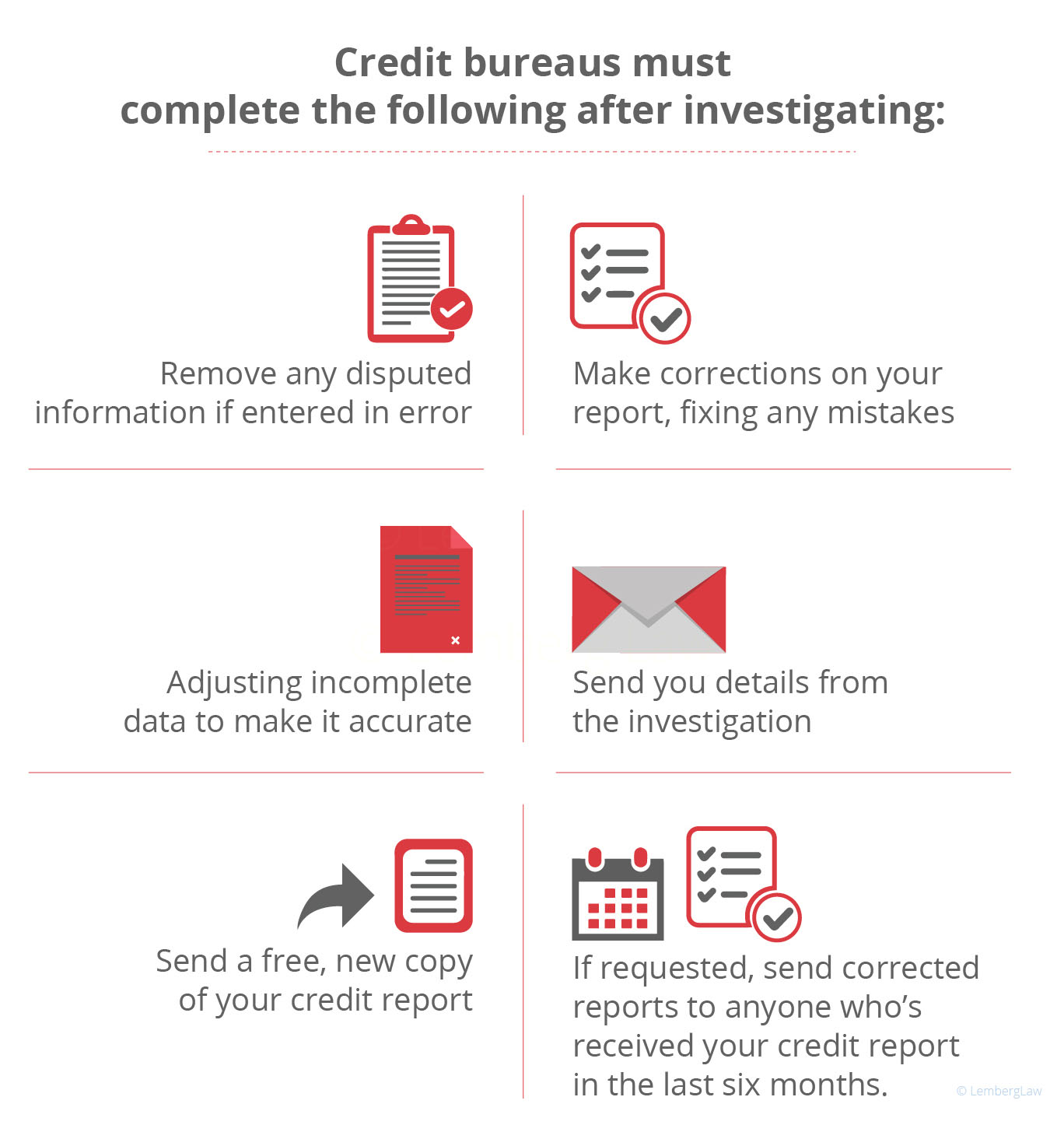

After completing your investigation, credit bureaus must complete the following:

They must remove any disputed information, provided it was proven to be entered in error or if it could not be confirmed. Such an instance like this would result from an account that belongs to someone else that hurts your file.

They must also make corrections on your report, fixing any mistakes.

They must correct any incomplete information, adjusting it to reflect accurate data.

They must send you details from the investigation. This would include a free, new copy of your credit report.

If you desire, they must send correction reports to any party who’s received your credit report in the last six months. They must also send out, should you request it, corrected copies to any employers who have requested it in the previous two years.

When attempting to have your errors fixed, make sure also to send a letter to the creditor. You’ll want to make sure you follow the same guidelines you did for submitting corrections to the credit bureau. Be aware that creditors often have different addresses for disputes. Once they have received your letter, the information provider must then include a notice of your dispute in any report sent to the credit bureau.

Should any information that was previously deleted turn out to be accurate, the bureau can place this information back into your file. They must provide you with a written notice, however. And this notice must include the name, phone number, and address of the contact for the information.

Correct but Damaging Details

Time is the only factor that can remove damaging details. These details remain on your report for seven years until they are finally removed, according to the FTC. There are exceptions, however:

Criminal Convictions Do Not Have Exceptions.

There Is a 10 Year Limit on Bankruptcy Information: If you apply for a job with a salary above $75,000 or if you apply for a credit line life insurance of more than $150,000 then there are no limits for this information.

Lawsuits or Unpaid Judgments: These can be reported for seven years or until the statute of limitations finishes. It depends on which is longer.

Submitting Additional Information

Many other companies don’t provide information to your credit report. However, you can ask to add this information. This can include local retailers, credit unions, gasoline card companies, travel, and entertainment companies as well.

If it was determined that you have “no credit file” or an “insufficient credit file,” then it is important to know you can submit more information. Any accounts that are in good standing, but that doesn’t appear on your report, can be added to your file.

Credit bureaus may charge a fee, as they are often not required to do this. One last thing to keep in mind: the file may not be updated if the creditor does not regularly report to the bureau.

What Can You Do If a Credit Bureau Won’t Solve a Dispute?

If after all your efforts, your dispute remains unsolved, you should write a letter detailing your dispute and mail it to the bureau, requesting it be placed with your file as well as in future reports. And if you believe that the bureau has violated the law, you have the right to sue them. You also have the option to report them to your state’s Attorney General and the FTC.

Reach Out If You Need Help

If you or someone you care about has a dispute over a credit report get in touch with the Lemberg Law legal team. Our lawyers have experience helping victims of credit errors. Complete our form for a FREE case evaluation, or call 844-685-9200 NOW. We can help you through the process. Should it turn out that the bureau has violated the law, you may be entitled to compensation.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."

I am trying to determine at what point can I hold the CRA’s liable for inaccurate reporting of a debt?