Overdrafts occur when a customer makes a transaction using more funds than currently available in his or her checking account.

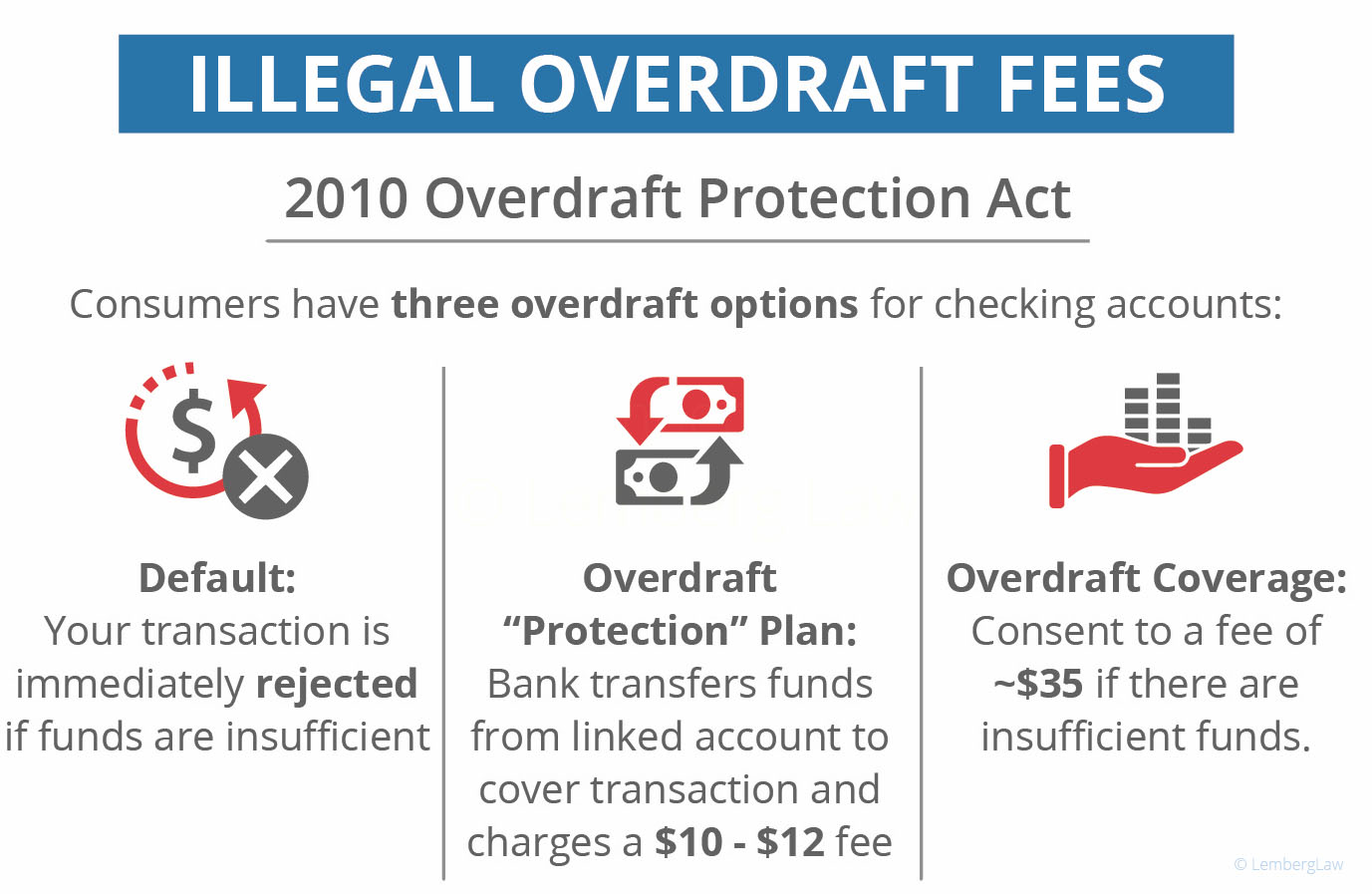

Currently, under the 2010 Overdraft Protection Act, customers have three options regarding overdrafts for a checking account:

Default: Do not opt into any plan, and have your transaction immediately rejected by the merchant in the event of insufficient funds.

Opt-in to overdraft coverage, consenting to a fee of ~$35 when the bank process any transaction resulting in a negative account balance.

Opt-in to an “Overdraft Protection Plan” whereby the bank processes the negative transaction and transfers funds to the linked account for a fee of ~$10-$12. Requires sufficient funds or qualifying line of credit in order to execute.

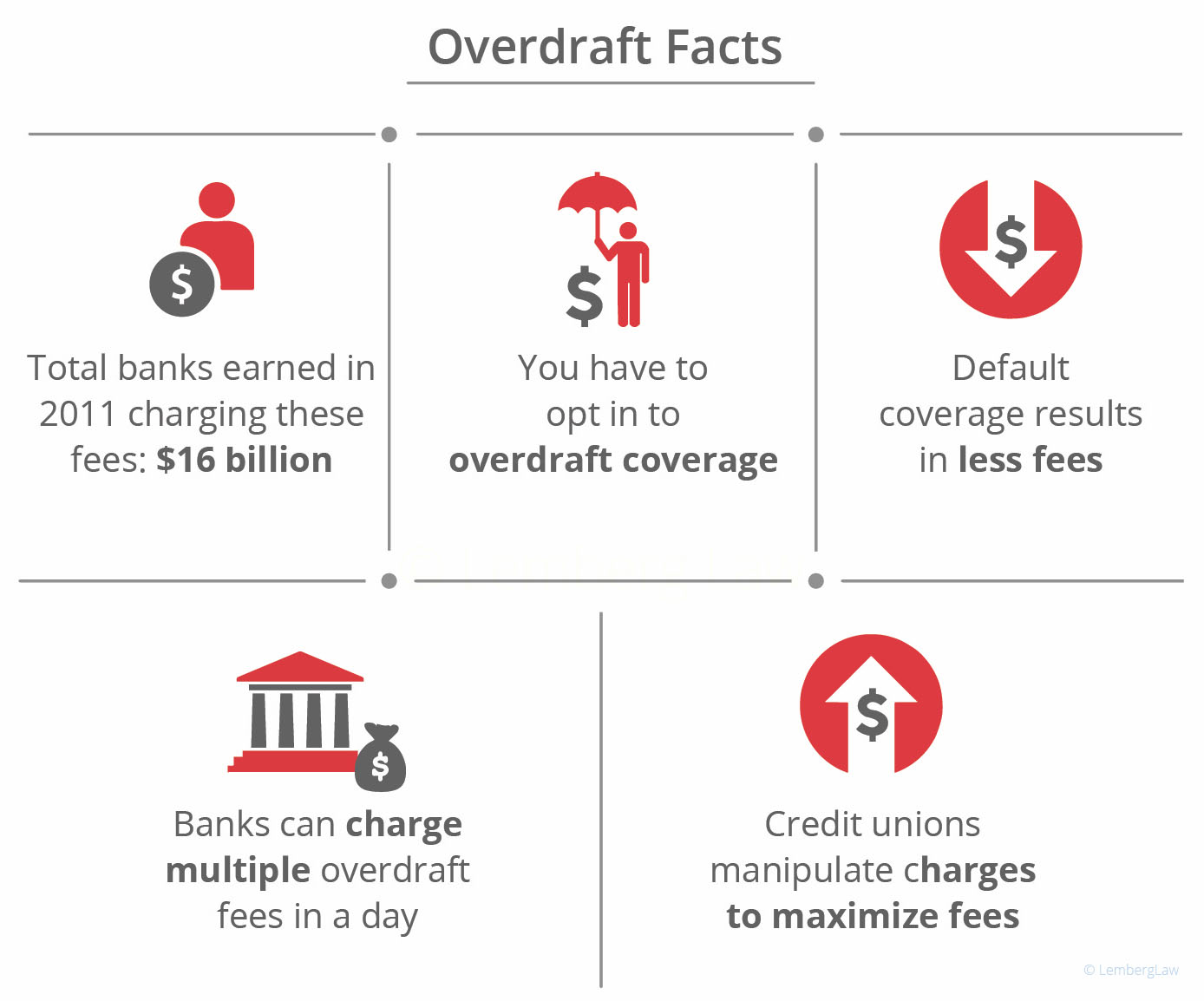

Although consumers now have these (not exactly favorable) options available to them, heavy marketing campaigns by banks and a lack of transparency have resulted in a dearth of financial literacy regarding overdraft fees. Even further, despite already executing these seemingly exorbitant fees (totaling $16 billion in 2011), credit unions still attempt to manipulate purchases and terms in order to trigger fees an increasing rate.

Common Strategies Credit Unions Use to Trigger Unfair Overdraft Fees

Reordering Transactions

Rather than debit a customer’s account in the chronological order, the transactions were made, the credit union will instead process the debit in highest-to-lowest order, thereby maximizing the number of overdraft fees it can charge. For example, assume you have $100 in your account. You then stop and make three small, separate purchases for $10, $12, and $18. Then, you go to the supermarket and buy groceries for $50. Lastly, you stop for gas on your way home and debit $40. If these purchases were processed chronologically, as they were executed in real time, you would only be charged for one overdraft fee. However, some credit unions process these fees in a business day according to value, from highest to lowest. Therefore, in this example, you would be charged for twice in lieu of once.

“Extended” or “Sustained” Overdraft Fees

Some credit unions charge additional fees to customers who fail to replenish their accounts within a certain window of time, usually 7-10 days, after triggering a negative account balance. Earning the title “extended” or “sustained” overdraft fees, these charges are distinct from the original overdraft fee and therefore functionally equivalent to an interest payment. Since the National Bank Act regulates the upper limit on how much a business can charge in interest, and many of these fees exceed 50x the limit, there have already been several lawsuits related to this practice.

Fees on everyday consumer purchases

Finally, some banking institutions are in direct contravention to initiatives that stipulated they would only charge overdraft fees on specific debit card transactions, namely recurring transactions (such as monthly student loan or mortgage payments). However, it’s suspected that many credit unions are levying overdraft fees on everyday purchases even when consumers have opted into contracts that specify otherwise.

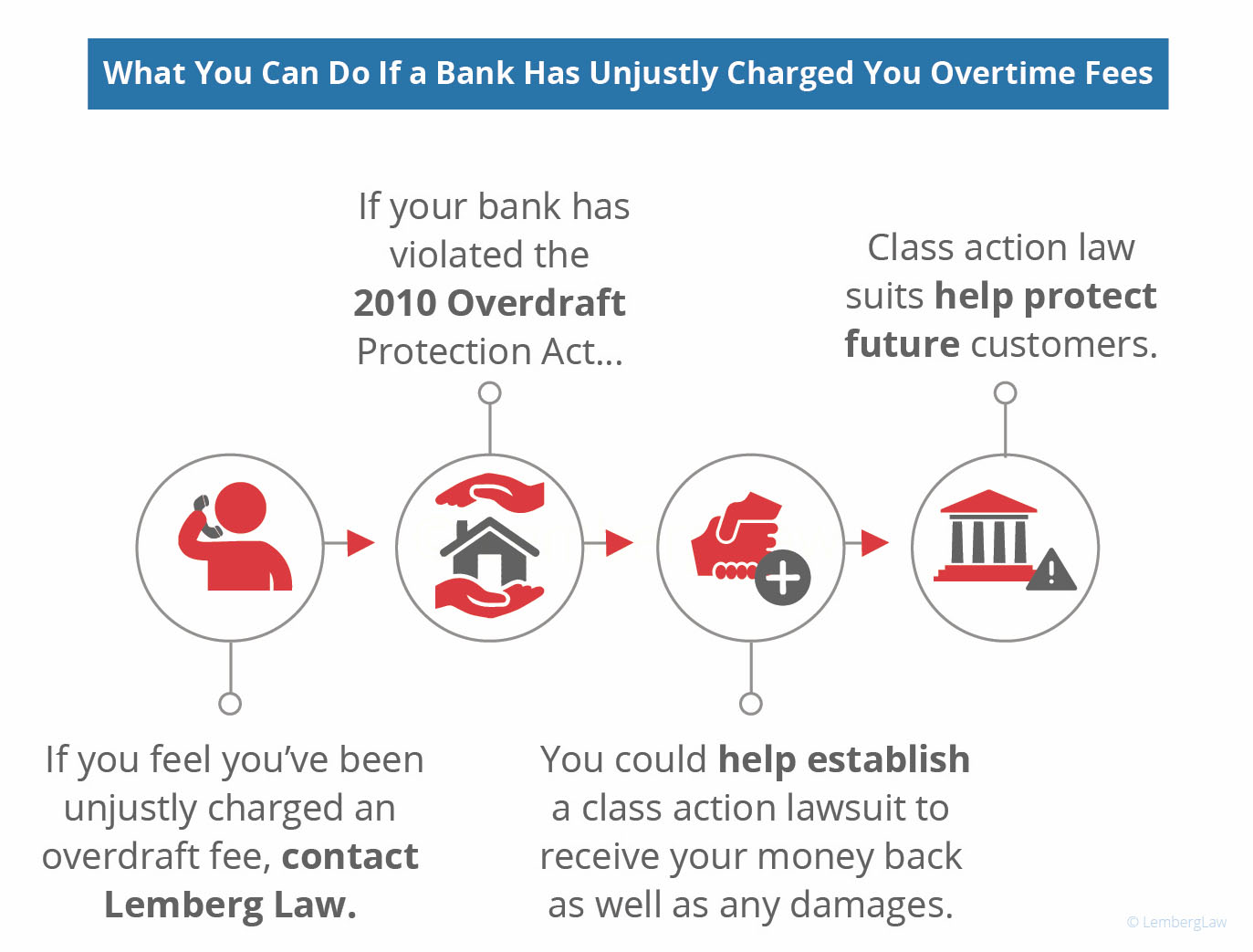

In establishing a class action lawsuit, Lemberg Law hopes to get consumers their money back, as well as just compensation for their troubles. Additionally, prosecuting offending institutions can serve as a prophylactic for future infractions.

If you believe that your credit union is using any of these tactics, or doing something else that seems illegal, tell us about it by filling out our form or calling us now at ☎ 844-685-9200. Our experienced attorneys handling this investigation can help you directly, and ensure that you receive the justice you deserve.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."

THANK YOU for your consumer advocacy representation & support! We need it! Overdraft fees are just another revenue-generating instrument undermining consumers’ financial stability & success. Just that many financial institutions have eliminated those fees says they’re simply another profit stream. A big one! Whether it’s overdraft fees or credit reporting- it’s abundantly clear- as a consumer- it’s definitely more beneficial to err on side of “businesses” than do right by consumers.

Roxanne T

Credit Union caused me to lose my insurance account. charging me so many overdraft fees

Crystal C

I had money in my account with the pending payments being just a couple of dollars less then the balance however I forgot a auto payment and it would have overdrawn my account that’s fair however my credit Union overdrafts with fees every pending payment even though the money was there.

THANK YOU for your consumer advocacy representation & support! We need it!

Overdraft fees are just another revenue-generating instrument undermining consumers’ financial stability & success. Just that many financial institutions have eliminated those fees says they’re simply another profit stream. A big one!

Whether it’s overdraft fees or credit reporting- it’s abundantly clear- as a consumer- it’s definitely more beneficial to err on side of “businesses” than do right by consumers.

Credit Union caused me to lose my insurance account. charging me so many overdraft fees

I had money in my account with the pending payments being just a couple of dollars less then the balance however I forgot a auto payment and it would have overdrawn my account that’s fair however my credit Union overdrafts with fees every pending payment even though the money was there.