Identity theft occurs when someone steals your personal information to commit fraud. The thief may use your information to apply for credit, file taxes, or get medical services. When this occurs, it could damage your credit status and cost you time and money to fix the damages.

Identity theft can have severe consequences on one’s finances. The Consumer Sentinel Network, maintained by the Federal Trade Commission (FTC), found that consumers lost more than $1.9 billion to identify theft and fraud in 2019 – an increase of $293 million over what was reported in 2018.

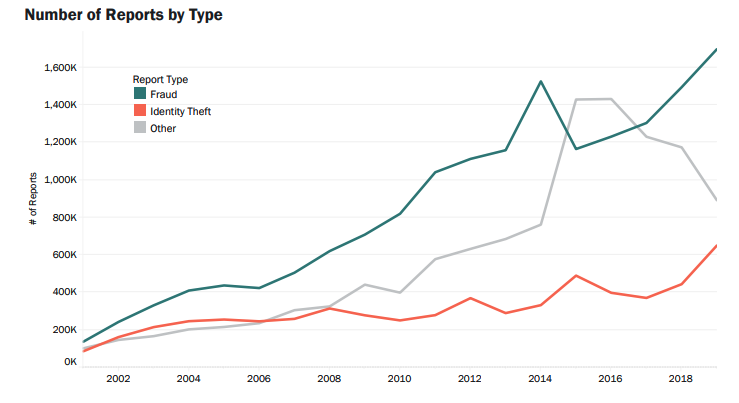

In 2019, people filed more reports about identity theft than any other type of complaint. Credit card fraud topped the list of identity theft reported in 2019. The FTC received more than 271,000 reports from people “who said their information was misused on an existing account or to open a new credit card account.”

The Fair and Accurate Credit Transactions Act of 2003, which amended the Fair Credit Reporting Act (FCRA), added provisions to improve the accuracy of consumers’ credit-related records and help consumers combat identity theft.

For example, the FACT provides consumers “the right to one free credit report a year from the credit reporting agencies, and consumer may also purchase, for a reasonable fee, a credit score along with information and how the credit score is calculated.” The act also allowes consumers to place fraud alerts in their credit files, according to the Federal Trade Commission.

Identifying incorrect information on your credit report, such as accounts or addresses you don’t recognize, is a common warning sign of identity theft.

You can use your one free credit report a year to check for any suspicious activity on your report. If you see something that doesn’t look right, you can contact one of the three credit bureaus to add a fraud alert. A fraud alert adds additional verifications on your account, making it harder for an identity thief the open up more accounts in your name.

To reduce your risk of identity theft, you should:

Regularly review your bank and credit accounts

Safeguard your social security number

Use strong passwords and an authentication step

Watch your mailbox for stolen mail

Shred any credit card, bank, or investment statements that someone could take out of the garbage

Monitor your financial and medical statements.

FAQs about Identity Theft & Credit Reports

What is a fraud alert?

A fraud alert can add an extra level of security for free on your credit report. It adds additional verifications on your account, making it difficult for an identity thief to open up more accounts in your name.

How do I place a fraud alert on my credit report? How do I know which fraud alert is right for me?

To place a fraud alert, you have to first contact one of the three credit bureaus (Experian, Equifax, or TransUnion) and ask to put a fraud alert on your credit report. The credit bureau you contact with alert the other two credit bureaus. The credit bureau is also required by FACT to provide you with a list of your rights as consumers.

If you choose to add an initial fraud alert due to a suspicion of identity theft, the alert will stay on your report for one year and you can get a new alert after a year. If you have been a victim of fraud and have an identity theft report, you can add an extended fraud alert that will remain on your report for 7 years.

No. A fraud alert will not affect your credit score.

What should I do if my identity has been stolen?

The Federal Trade Commission outlines four steps you should take if you’ve been the victim of identity theft:

Place a fraud alert on your credit reports and review your credit reports. You only have to contact one consumer reporting agency (Experian, Equifax, or TransUnion); the law requires one credit bureau to notify the others in the event of identity theft. Each of the credit bureaus will send you a free copy of your credit report.

Close the accounts that you know, or believe, have been tampered with or opened fraudulently. Follow up with written notifications and supporting documents (but send copies, not originals). Send your notifications via certified mail, with return receipts requested.

File a report with your local police or the police in the community where the identity theft took place and ask for a copy of the police report. This will help you establish proof of identity theft.

If I am a fraud victim, do I have to pay for a credit report?

No. The Fair Credit Reporting Act says that a consumer who has reason to believe that information in their report is inaccurate due to fraud is entitled to a free copy of his or her credit report.

How can Lemberg Law help me?

The attorneys at Lemberg Law realize how emotionally and financially difficult it can be when you’re a victim of credit report or identity theft issues. Lemberg Law will stand by you throughout the process and help you get the justice you deserve. Call us at 475-277-2200 or complete our online form to receive a free, no-obligation consultation from our experienced legal team.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."