First, you learn that some thief stole your identity. Second, as you begin to recover, a debt collector calls. She wants payment on a credit card debt. Although your name is on the card, you know nothing about the card nor the thousands of dollars of purchases made by the thief. For what it is worth, you are not alone. In 2016, identity theft struck a record 15.4 million Americans causing $16 billion in losses, according to the Javelin Strategy Research “2017 Identify Fraud Study”.

Federal and state laws were written to protect identity theft victims from debt collector harassment. This article will explain the procedure which, if followed by you, will remove the legitimate debt collector from your life. It also will describe how to protect yourself from harassment by the unscrupulous debt collector who most likely works for a debt buyer.

Consider the classic example of Mr. X, an identity theft victim. A debt collector demanded payment of a $56,000 student loan. With assistance, Mr. X convinced the legitimate debt collector that the loan was not his. After two years, an unscrupulous debt collector contacted him about the loan. This debt collector had purchased this loan along with thousands of other loans. The debt collector sued Mr. X. Mr. X and his attorney appeared in court and demanded proof that the loan belonged to Mr. X. As is often the case, the debt buying debt collector had no proof. The case was dismissed. Mr. X collected damages from the debt collector for harassment.

What Is Debt Collector Harassment and How Can an Identity Theft Victim Avoid it.

The Federal Debt Collection Protection Act (FDCPA), administered by the Federal Trade Commission, defines illegal collection procedures. Many states have similar laws. The FDCPA specifically forbids these collection activities likely to harass, oppress, or abuse a consumer regarding the collection of a debt such:

Communicating improperly with third parties about your debt

Harassing or abusing you by threats, repeated phone calls or electronic contacts, or profanity

Making false or misleading representations

Using unfair practices

The FTC also has helpful online guidelines and a recovery plan for the identity theft victim. It recommends that, as your first step, you file an identity theft report online with its IdentityTheft.gov site. This site contains a list of actions to take to protect your rights. You have the right to:

Stop creditors and debt collectors from reporting fraudulent accounts. After you give them a copy of a valid identity theft report, they may not report fraudulent accounts to the credit reporting companies.

Get copies of documents related to the theft of your identity, like transaction records or applications for new accounts. Write to the company that has the documents, and include a copy of your identity theft report. You also can tell the company to give the documents to a specific law enforcement agency.

Stop a debt collector from contacting you. In most cases, debt collectors must stop contacting you after you send them a letter telling them to stop.

Get written information from a debt collector about a debt, including the name of the creditor and the amount you supposedly owe. If a debt collector contacts you about a debt, request this information in writing.

The FTC provides a sample of the letter to the debt collector. Use this letter to request detailed information about the account which may become proof that this account does not belong to you. It also requests that the debt collector no longer contact you.

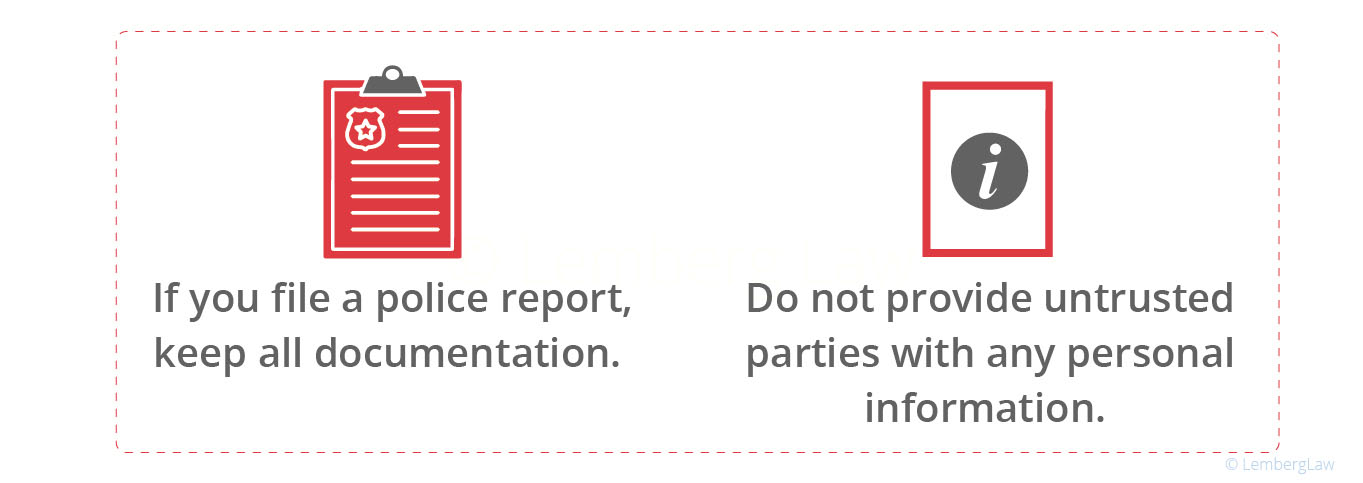

You may want to file a report with the police. You must keep all records and documents related to efforts to clear your name and re-establish your credit. Document every call or electronic message. Do not provide personal information unless you know the requesting party.

A reputable debt collector will honor your request for no further contact and will not continue collection proceeding unless it has evidence that the debt belongs to you. However, this debt may be sold to a debt buyer who likely will attempt to collect.

What Is a Debt Buyer and How Does an Identity Theft Victim Stop This Debt Collector?

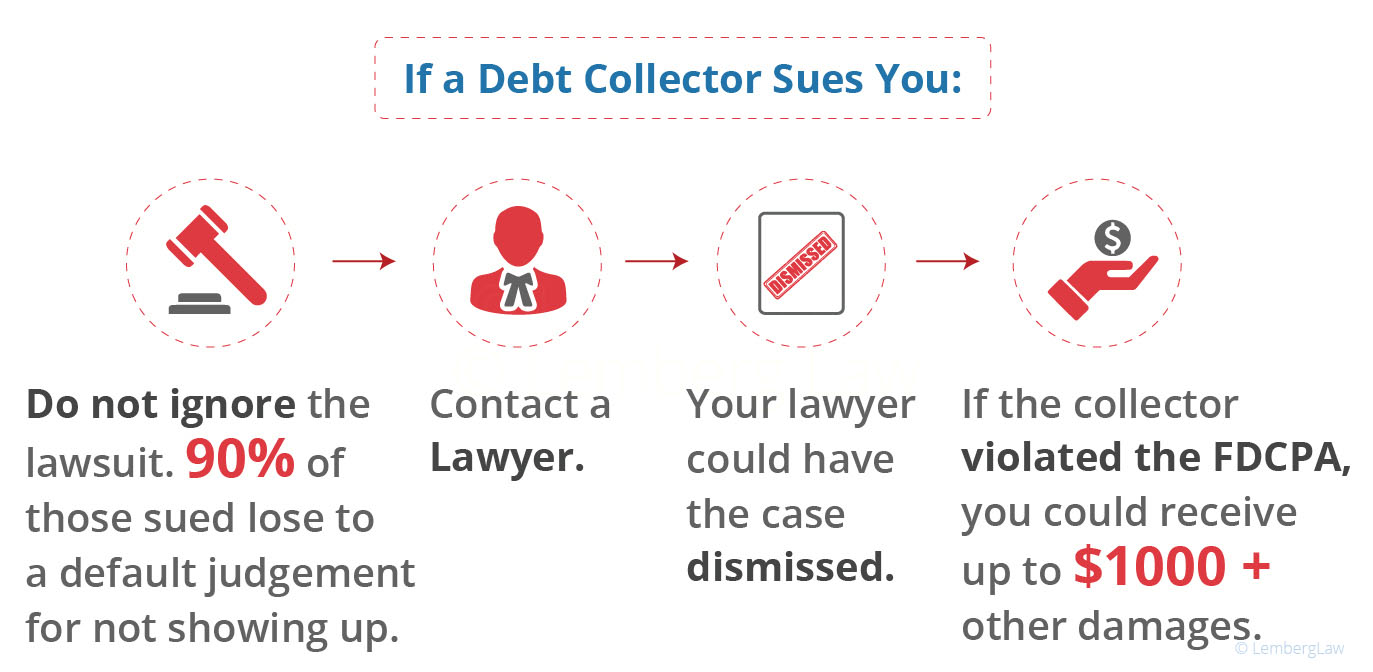

A debt buyer purchases thousands of old, uncollected debts for pennies on the dollar and makes money by collecting them from identity theft victims. He may harass you to collect or file a lawsuit to collect. If you are sued, immediately take the papers to an experienced consumer lawyer. If you ignore this lawsuit, the debt collector likely will get a default judgment against you, which may allow him to garnish wages, levy on your bank account, and put a lien on your property. As many as 90% of those sued do nothing. Do not be one of those who let the debt buyer win by default. If the debt collector lacks proof that the debt is yours, your lawyer may be able to get the case dismissed.

If a debt collector has been hounding you, speak with a representative directly by immediately calling 844-685-9200 for a free, no-obligation case evaluation. Our attorneys have experience in fighting debt collectors and standing up for consumers. If a debt buyer has violated the Fair Debt Collection Practices Act, you’re entitled to file suit in federal court and could be awarded up to $1,000 and other damages.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."

First, you learn that some thief stole your identity. Second, as you begin to recover, a debt collector calls. She wants payment on a credit card debt. Although your name is on the card, you know nothing about the card nor the thousands of dollars of purchases made by the thief. For what it is worth, you are not alone. In 2016, identity theft struck a record 15.4 million Americans causing $16 billion in losses, according to the Javelin Strategy Research “2017 Identify Fraud

First, you learn that some thief stole your identity. Second, as you begin to recover, a debt collector calls. She wants payment on a credit card debt. Although your name is on the card, you know nothing about the card nor the thousands of dollars of purchases made by the thief. For what it is worth, you are not alone. In 2016, identity theft struck a record 15.4 million Americans causing $16 billion in losses, according to the Javelin Strategy Research “2017 Identify Fraud

The FTC provides a

The FTC provides a