The economic impact of COVID-19 has left millions of American families facing difficult and unprecedented financial situations. Americans hit hardest by the pandemic are also members of the same populations that debt collectors tend to target, including low-income individuals, people of color, immigrants, and young people.

In March, a number of civil rights, racial and economic justice, labor, and community groups posted a letter addressed to New York Governor Andrew Cuomo and New York Chief Justice Janet DiFiore calling on federal and state governments to halt private and public debt collection to protect the public health, safety, and financial security of New Yorkers.

“Experts have warned that COVID-19 will disproportionately harm New Yorkers in low income communities and communities of color, as a result of widening health disparities, lack of benefits, financial insecurity, and other inequities,” the letter said. “These same communities disproportionately bear the brunt of fraudulent debt collection lawsuits, which are rampant, violate New Yorkers’ due process rights, and siphon massive amounts of wealth from and contribute to destabilization of entire neighborhoods.”

The letter featured numerous stories of women of color in New York whose safety and financial security were allegedly put at risk due to debt collectors during the pandemic. For example, the groups included the experience of Ms. M, a Black, single mother of three who lives in NYC public housing and works for a nonprofit. Ms. M discovered that her bank accounts were restrained because of a court judgement that was obtained without her knowledge in 2014.

Ms. M learned that the agency served the court papers at an address she never lived. Because her accounts were restrained and her next paycheck uncertain because of the pandemic, she had no money to pay her bills or prepare her family for the COVID-19 crisis. The agency to whom the alleged debt was owed refused to release her bank accounts unless she signed an agreement stating that she owed the debt.

Debt Collection and The Pandemic

Debt collectors may even act more aggressively during the pandemic, targeting and harassing Americans who are financially vulnerable. According to the Los Angeles Times, consumer advocates have said that debt collectors have grown increasingly aggressive as stay-at-home orders have made it easier for them to contact and sometimes harass people who owe debts.

Although the federal government sent stimulus checks and enacted protections against evictions, foreclosures, and federal student loans under the CARES Act, the seizure of wages for consumer debts that are not federal or state related continued.

For example, checks were not protected from private creditors from collecting debt on things like private student loans and credit card bills. Only a few states issued executive orders ensuring that the government’s stimulus checks were protected from garnishment. Generally, unemployment checks are protected from garnishment, but they can be at risk of being taken by the collector once they are deposited into bank accounts.

Lauren Saunders, an associate director at the National Consumer Law Center, told MarketWatch in May that banks who are “presented with a garnishment order are likely to freeze amounts in the account and give the consumer a short time to prove in court that account funds are exempt from seizure — a daunting prospect at any time, and a near impossibility today when many courts are at least physically closed, people are ordered to stay at home, and attorneys are inaccessible.”

COVID-19’s Impact on Black, Latinx & Immigrant Businesses

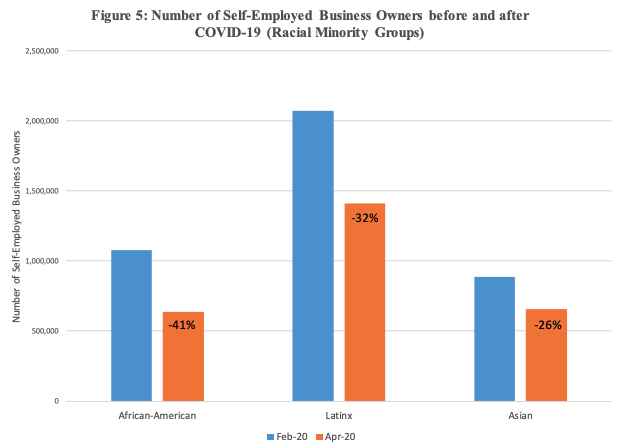

A report published by the National Bureau of Economic Research found that African American business owners were hit the hardest by COVID-19. The number of African American business owners declined from 1.1 million in February 2020 to 640,000 in April 2020.

Latinx business owners also experienced major losses – the number of Latinx business owners decreased 32% from February to March. Asian business owners suffered losses of 26% and immigrant business owners experienced loses of 36%.

Number of Self-Employed Business Owners Before and After COVID-19 (Racial Minority Groups)

Robert Fairlie, an economics professor at the University of California, Santa Cruz, and lead researcher on the report, expressed concern with the report’s findings and the overall impact the numbers can have on broader racial inequality moving forward.

“The negative early-stage impacts on minority- and immigrant-owned businesses, if prolonged, may be problematic for broader racial inequality because of the importance of minority businesses for local job creation,” Fairlie said in the report. Overall, Fairlie found that the pandemic had accounted for the loss of 3.3 million business owners.

The pandemic also caused consumer debt to nationally plummet across housing and non-housing debt. According to the Federal Bank of New York quarterly report, credit card balances fell by $76 billion in the second quarter, reflecting the decline in consumer spending due to the COVID-19 pandemic and social distancing. Non-housing debt, including credit card, auto loan, student loan, and other debts, saw a $86 billion decline – the largest decline in the report’s history.

Although consumer debt decreased for American’s nationally, experts said that financial protections passed by the federal government may be hiding the true financial distress of many American families and individuals.

Joelle Scally, Administrator for the Center for Microeconomic Data at the Federal Reserve Bank of New York, said in a statement that the temporary relief measures, such as the CARES Act, may “mask the very real financial challenges that Americans may be experiencing as a result of the COVID-19 pandemic and the subsequent economic slowdown.”

Know Your Rights as Consumers

Under the Fair Debt Collection Practices Act, debt collectors are prohibited from using threatening, harassing, or intimidating language. For example, they cannot threaten to sue you or garnish your wages unless they actually intend to do so. Debt collectors cannot speak to third parties, such as family members, about the debt itself, unless they are associated with the debt. Debt collectors are only permitted to ask for the name, address, and telephone number of the person authorized to pay the debts.

To stop a debt collector from calling, you need to file a cease and desist letter stating that you no longer want to receive calls from the collector. The collector can only contact you to confirm that there will be no further contact or that the creditor plans to take a specific action, such as to garnish your wages or file a lawsuit. If you want to stop wage garnishments, you must file a claim of exemption by filling a document with the court that issued the garnishment order.

Navigating debt collectors who may be at fault can be a scary and frustrating experience, but it doesn’t have to be. For 13 years, Lemberg Law has made legal representation a pain-free and easily accessible process. We have successfully recovered more than $50 million in damages for more than 25,000 clients across the nation. Our track record speaks for itself.

Call Lemberg Law at 475-277-2200 or use the case evaluation form on our website to receive a free, no obligation consultation from our experienced legal team.

FAQs about Debt Collection & COVID-19

Are stimulus checks protected from wage garnishment?

The CARES Act does not explicitly state that stimulus payments are exempt from garnishment. Only a few states, like Massachusetts, have issued executive orders to stop garnishment orders. Some local court system also has determined they will not accept requests from debt collectors. It is important to review your state laws and determine if your state or local government has issued emergency orders to stop all or some garnishment orders.

What are some wage garnishment exemptions? How can I file a Claim of Exemption?

Wage garnishment exemptions prevents creditors from garnishing certain kinds of income or more than a certain amount of your wages. Each state has different exemption laws to protect you wages. Some types of wages that are generally fully exempt include: social security, disability, retirement, child support, and alimony.

Wages are subject to garnishment unless you claim an exemption. To do so, you must file a claim of exemption by filling a document with the court that issued the garnishment order. In the form, you must explain why or all of the wages the creditor wants your employer to garnish should be exempt from being taken. You must file the completed document with the court office where the garnishment originated.

Can a debt collector contact anyone else about my debt?

A debt collector can’t discuss your debt with anyone but you or your spouse, or an individual who is associated with your debt. A collector is permitted to call other people, such as your relatives, to find out contact information, such as your address, your phone number, and where you work.

Are there limits on when a debt collector can call?

The FDCPA prevents debt collectors from calling at “any unusual time or place or at a time or place known or which should be known to be inconvenient to the consumer.” The FTC says, “Depending on the circumstances, contacting survivors about a debt shortly after the debtor dies may be unusual, inconvenient, or both.” In other words, if a debt collector repeatedly calls a family member in the midst of bereavement, it could be a violation of the FDCPA.

How do I get a debt collector to stop calling?

You must send a cease and desist letter to the collector stating that you do not want the collector to contact you again. Make sure to keep a copy of the letter for your records. Once the collector gets your letter, he cannot contact you again except to confirm that there will be no further contact or that he or the creditor plans to take a specific action, like filing a lawsuit to collect the debt. The Consumer Financial Protection Bureau provides sample letters to help if you’re experiencing common problems with debt collectors.

What will the process look like if I file with Lemberg Law?

You can call us at 475-277-2200 or use our case evaluation form to receive a free, no-obligation consultation from our experienced legal team. If your case is accepted, we work toward a settlement or take the responsible party to court. If we win, you receive the compensation you deserve. If we don’t prevail in the case, we cover the tab for you.

About the Author:

Sergei Lemberg is an attorney focusing on consumer law, class actions related to automotive issues, and personal injury litigation. With nearly two decades of experience, his areas of practice include Lemon Law (vehicle defects), Debt Collection Harassment, TCPA (illegal robocalls and texts), Fair Credit Reporting Act, Overtime claims, Personal Injury cases, and Class Actions. He has consistently been recognized as the nation's "most active consumer attorney." In 2020, Mr. Lemberg represented Noah Duguid before the United States Supreme Court in the landmark case Duguid v. Facebook. He is also the author of "Defanging Debt Collectors," a guide that empowers consumers to fight back against debt collectors and prevail, as well as "Lemon Law 101: The Laws That Lemon Dealers Don't Want You to Know."